Developers looking to tempt buyers are having to offer a range of incentives, such as flexible payment terms, to tempt buyers in what remains a soft property market.

Last week, Aldar Properties, the biggest developer in Abu Dhabi, rolled out a rent-to-own scheme at three of its developments in the Ansam, Al Hadeel and Meera communities, allowing customers to build equity in apartments with no rent escalations or additional fees. The developer said potential buyers entering rent-to-own schemes can build equity of 16 per cent, 19 per cent and 22 per cent over the first, second and third year of living in their apartments, with a rebate available if they decide to exercise an ownership option.

The Abu Dhabi-based developer said rents under the scheme start at Dh120,000 per year in Ansam, Dh140,000 per year in Al Hadeel, and from Dh110,000 in Meera.

Though rent-to-own is not new — such schemes have existed in the market since the early 2000s — they flourished after 2008 when the UAE’s property market slumped following a global economic crisis and developers were motivated to attract buyers, says Matthew Gregory, head of property sales at classified listings portal dubizzle.

It is clearly gaining popularity in 2019, with developers eager to explore new and creative ways to attract buyers, according to analysts.

“Rent-to-own schemes can offer those looking to buy property, with stable income but perhaps limited savings, an attractive way of working towards home ownership,” said Chris Hobden, head of strategic consultancy at Chestertons.

“The schemes also allow developers access to a broader range of potential buyers and can provide a competitive edge over units offered for sale through more conventional payment structures,” he said.

How does the rent to own scheme work? Do people need to pay extra as part of the scheme than they would do in renting a flat normally?

Schemes vary between developers although essentially they comprise a rental contract coupled with a future sales agreement, detailing a pre-agreed price and a fixed payment schedule.

Monthly payments would generally be above market rent, reflecting a capital contribution, although the premiums vary widely and are often marketed as equivalent to paying rent over the period.

Do customers need to make any down payment as part of the scheme?

There is often, though not always, a down payment required. This would be significantly lower than the down payment generally required for a mortgage.

________________

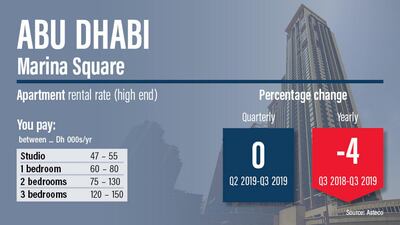

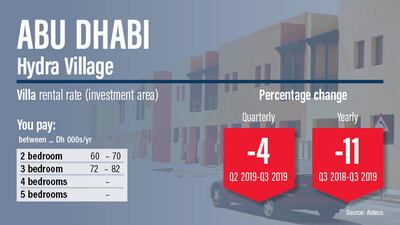

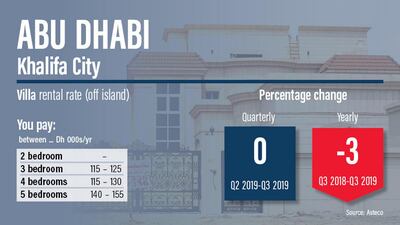

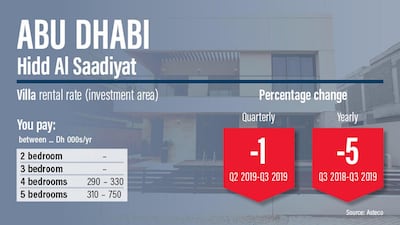

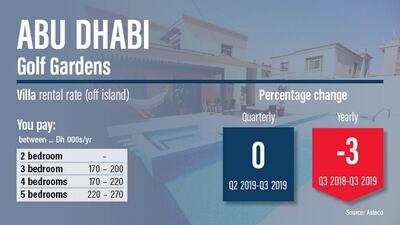

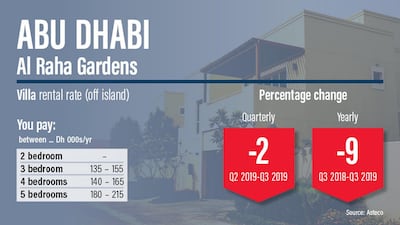

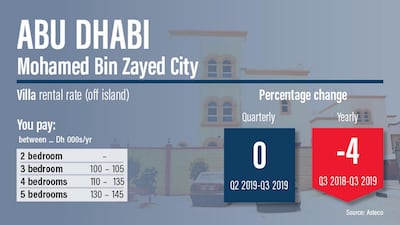

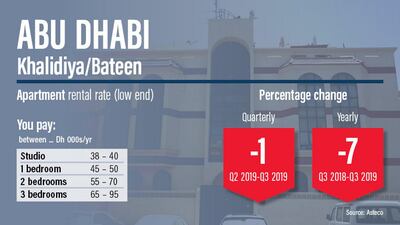

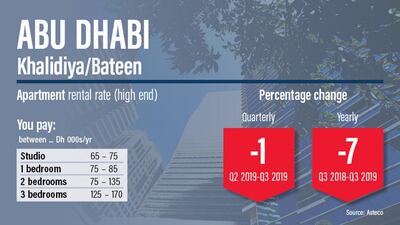

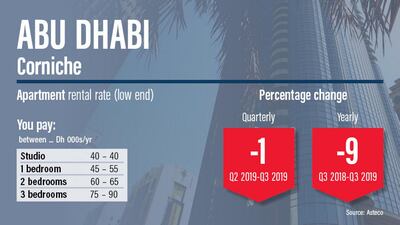

Abu Dhabi rents Q3, 2019

-

Ramon Penas / The National -

Ramon Penas / The National -

Ramon Penas / The National -

Ramon Penas / The National -

Ramon Penas / The National -

Ramon Penas / The National -

Ramon Penas / The National -

Ramon Penas / The National -

Ramon Penas / The National -

Ramon Penas / The National -

Ramon Penas / The National -

Ramon Penas / The National -

Ramon Penas / The National -

Ramon Penas / The National -

Ramon Penas / The National -

Ramon Penas / The National -

Ramon Penas / The National -

Ramon Penas / The National -

Ramon Penas / The National -

Ramon Penas / The National -

Ramon Penas / The National -

Ramon Penas / The National -

Ramon Penas / The National -

Ramon Penas / The National -

Ramon Penas / The National -

Ramon Penas / The National -

Ramon Penas / The National

________________

What are the advantages of this scheme?

Rent-to-own (RTO) schemes can offer those looking to buy property, with stable income but perhaps limited savings, an attractive way of working towards home ownership without the need for mortgage finance.

“The terms offered vary between developers and it is essential that those considering an RTO contract look carefully at the structure on offer,” says Mr Hobden.

Are there other developers in the UAE who have similar rent-to-own schemes like the one launched by Aldar?

"Prominent developers in the UAE such as Emaar are also adopting rent-to-own style schemes to open up their customer base to a new market of potential investors, however, the adoption of such schemes by more developers will support in driving the market forward," says dubizzle's Mr Gregory.

Is it possible to walk away from a rent-to-own scheme after starting payments?

Typically, yes, although the money paid over the rental period would generally be forfeited. Under some schemes, it may be possible to transfer the agreement to a third party.

Are banks ready to grant loans to people who are taking part in such a scheme?

Rent-to-own deals generally negate the initial need for bank finance, although some schemes will require a final lump sum payment.